On the 14th of April we provided an update on the banking sector following the down grade by Fitch Ratings of the four major banks and the introduction of the RBA’s Term Funding Facility (TFF).

The intent of the TFF was to achieve two objectives:

- to reinforce the benefits to the economy of a lower cash rate, by reducing the funding costs of ADIs and in turn helping to reduce interest rates for borrowers. It will complement the reduction in funding costs from the Reserve Bank’s target for three-year Australian Government bond yields; and

- to encourage ADIs to support businesses during a difficult period, ADIs will have access to additional low-cost funding if they expand their lending to businesses over the period ahead. The scheme encourages lending to all businesses, although the incentives are stronger for small and medium-sized enterprises (SMEs).

The TFF was varied on 1 September 2020 to provide further support, taking the total funding available to the ADIs at the rate of 0.25% to circa $200 billion or 5% of outstanding credit.

This flood of cheap funding together with relatively low levels of credit growth have caused the unintended consequence of effectively shutting down the very important short term money market.

There is a very large sector of the investment markets that rely on an active short term money market as a place to invest surplus money, regulatory liquidity and mandated funds. Investors such as universities, not-for-profits, local councils, charitable organisations, small ADIs and professionally run cash funds all rely on ADIs actively issuing wholesale term deposits and other senior debt products such as floating rate notes. These investment types are the result of conservative nature of investment policies or, in many cases, mandated by government legislation.

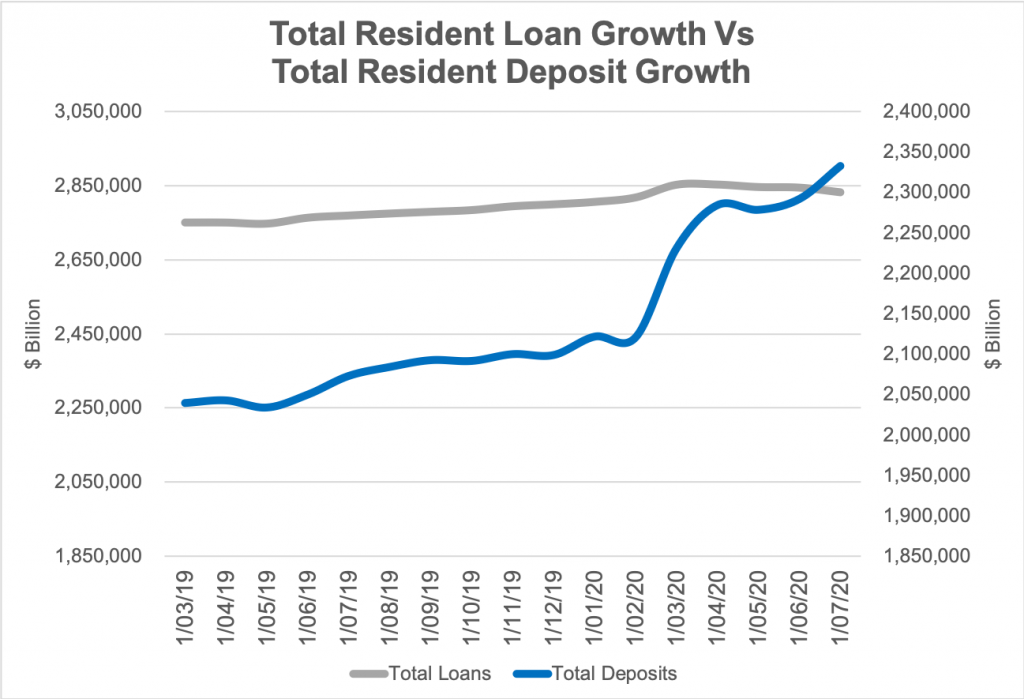

As at 30 June 2020, Australian ADIs had loan growth of 2.9% or $81 billion while deposit growth from households grew by 8.6% or $81.6 billion, deposits by non financial business grew by 15.3% or $87.6 billion and deposits by general government grew by 27.3% or $18.5 billion. Banks are simply swimming in liquidity. Cash and liquid assets were up 64.5% year on year 1.

The increase in TFF, which on current loan growth rates represents 2 years of cheap funding for the ADIs, exacerbates the problem for investors. ADIs have actively been running off wholesale deposits in favour of the cheaper funding on offer by the RBA. It is far easier to run off wholesale deposits than deposits to households, so the investor groups mentioned above are facing the unusual challenge of finding a bank willing to take their investment funds.

Given the wall of cash mounting on ADI balance sheets it is highly likely that we won’t see a new senior unsecured (FRN) issue from any of the banks for the foreseeable future and potentially as long as 12 months. This has led to a massive contraction in credit spreads as investors buy up any short dated FRNs that remain available in the secondary market.

We are also unlikely to see an active wholesale deposit market equivalent to pre-pandemic levels for the same period.

For many investment managers it’s no longer a question of which bank is showing the best rate, but which bank wants to take a deposit at all. Another cut in the official cash rate which is now largely factored into short term rates is further pain for investors who rely on interest income to help cover operational expenses.

So, what are the alternatives?

We think now is a great time to revisit investment polices to ascertain what changes can be made to take advantage of available investment options.

There are many foreign banks that are active in the wholesale term deposit market who have not been eligible for TFF funding and are still actively sourcing deposits. Other investment types such as short dated corporate commercial paper, RMBS and ADI issued subordinated debt all still offer good risk adjusted returns when overlaying investment regulations allow.

As a manager/advisor of over $3.5 billion of conservative cash style portfolios and $3.6 billion of securitised assets, Laminar Capital is experienced in helping investors review policies and finding alternatives. Please reach out if we can help in this regard.